Blockchain might sound like a complex idea when you hear it for the first time. Sure, the technicalities are indeed tricky, but the concept is not that hard to grasp. Think of blockchain as a data repository or database.

A database holds an array of electronic data. As a repository, a database contains large amounts of data and allows multiple users to access, filter, and process data simultaneously. To facilitate faster sorting and get query results quickly, data in databases are in tabulated format.

Blockchain versus database

The database primarily differs from the blockchain in terms of data format. A blockchain arranges information in blocks. Please take note that each block has a specific storage space; it gets filled over time. When that happens, this block is connected like a chain to the formerly filled block. This chain connection of blocks led to the invention of the term “blockchain.”

As presented in the preceding, databases arrange data into tabular formats while a blockchain forms a chain of blocks. Blockchain creates a permanent timeline of data if not centralized. Every time a block gets filled and attached to the blockchain, it forms part of the blockchain for good and gets a specific timestamp.

Uses of blockchain

Blockchains hold information related to financial transactions. However, as the technology develops, users realize that blockchains can carry other types of data.

Banking

Banks can significantly benefit from blockchain integration into the banking system. Banks are open during weekdays only, that is, five days a week. In contrast, blockchain runs 24/7. With blockchain integration, banks can handle transactions in at least ten minutes without regard to the time of day and even during weekends and holidays.

Currency

Blockchain underpins Bitcoin and altcoins. Blockchains employ a group of computers to run the platform. Through this system, blockchain permits Bitcoin and altcoins to run even without a controlling authority. This system reduces not only the security risks but also the costs involved in performing financial transactions.

Healthcare

Health institutions can harness the blockchain in securely keeping medical records of patients. When a healthcare professional produces and approves a medical record, he can encode the record in the blockchain. Handling medical records in this manner ensures the integrity of such records.

Property rights

Property recording is both time demanding and costly. In addition, it is prone to human error, which can make property ownership identification difficult. With blockchain, there is no need to scan documents and locate physical files manually in cabinets. Once the personnel in-charge encodes data and the network verifies the property ownership, the system can guarantee the accuracy of the deed and the integrity of recorded data.

Smart contracts

While the term sounds complicated, you can quickly assimilate the idea behind smart contracts, which are codes that developers can build into the blockchain. Smart contracts exist to enable, authenticate, or come up with an agreement. The parties to the agreement must agree to the conditions set out in the contract. When all conditions are satisfied either by one or both parties, the system will automatically carry out the terms in the agreement.

Supply chains

Companies can utilize the blockchain to keep a listing of purchased materials and their origins. This will enable manufacturers to confirm that their products are authentic. At this time, there is an increasing trend within the food industry toward blockchain acceptance. The purpose is to know the stop points where the food changes hands until it reaches the end-user.

Voting

A voting system can incorporate blockchain to achieve an efficient voting process. With blockchain, it is possible to eradicate election fraud and promote voter participation. With this system, it is next to impossible to alter the votes fraudulently.

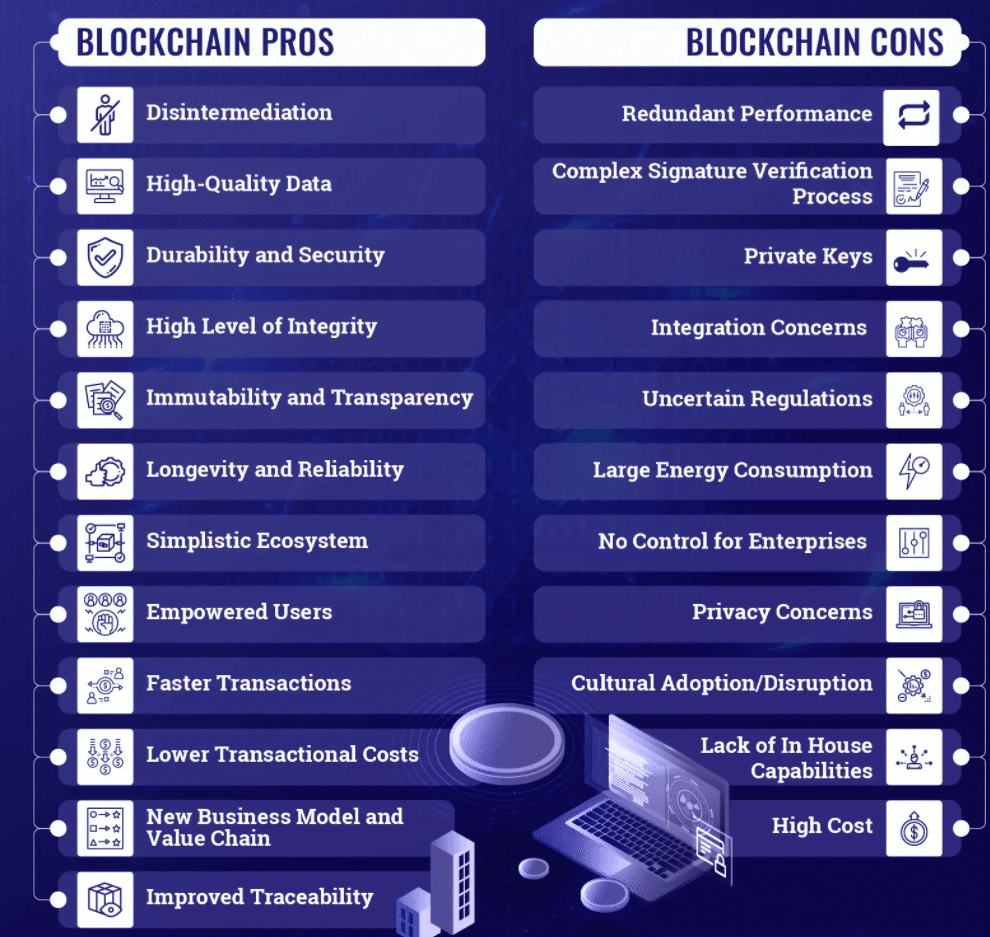

Pros and cons of blockchain

Blockchain has a lot of potential in terms of storing data. It might see other uses in the future apart from what has been presented thus far. However, there are pros and cons of blockchain that the user must be aware of.

Upsides of blockchain

Let us discuss the upsides of blockchain first.

- Accuracy

Whenever someone enters a transaction, all computers in the network, which may count to thousands, will review and confirm the transaction. Therefore, human involvement is almost zero during verification. As a result, human error is out of the window, and users are confident that recorded information is accurate.

- Reduced cost

Performing any type of transaction involves a fee. For example, you will pay an attorney when you have a legal document notarized, a church minister to administer a wedding, or a bank when you check your account balance from an ATM unless you use one from your bank. Blockchain removes the necessity to perform third-party authentication, saving the user money in the process.

- Decentralization

Blockchain does not put data in one central location. Instead, a group of computers maintains an identical copy of the blockchain. When one computer adds a new block to the blockchain, all of these computers update their blockchain copy to keep one copy.

- Efficient transactions

Financial transactions handled the traditional way can take several days to complete. While financial institutions typically operate during weekdays, blockchain is running 24/7, around the clock, and throughout the year. Through blockchain, transactions are completed in a matter of ten minutes and become final a few hours later.

- Confidential transactions

Several blockchain platforms work as public databases. Therefore, anyone with internet connectivity can visit the platforms’ websites and see a list of transactions. While users can see some transaction details, they cannot see the parties involved in the transactions. Instead of thinking about crypto transactions as anonymous, you can use the more relevant term confidential.

Downsides of blockchain

Blockchain indeed brings about a lot of positive changes to the world. However, its adoption does not follow a straight path. There are resistances along the way. The challenges involved in accepting this new technology are technical and regulatory, and political. Below are among the roadblocks encountered by blockchain toward widespread acceptance.

- Cost of technology

While blockchain will allow you to save money on processing fees, the technology is still not free. You may not pay money out of pocket directly, but you will use electricity and computer resources when you do blockchain transactions. In reality, the amount of electricity consumed by computers running on the Bitcoin network is almost equal to the annual electricity usage of Denmark.

- Inefficient speed

Blockchain is still inefficient at present, and this is more evident in BTC. It takes more or less ten minutes to attach a new block to Bitcoin’s blockchain. Therefore, the Bitcoin network can facilitate only seven transactions, on average, per second. Meanwhile, some blockchains boast a processing speed of 30,000 transactions in the same period.

- Illegal activities

Although blockchain preserves users’ privacy while conducting business on the platform, this attribute is a double-edged sword. Confidentiality in transactions makes way for the perpetration of illegal activities online through the platform.

- Regulation

Many crypto users are wary about the possible intervention of the government on cryptocurrencies. Because decentralization in Bitcoin, for example, has dramatically expanded, it becomes rather challenging or almost impossible for regulators to apply the brakes and bring this digital currency to a stop.

Still, if it wants to, the government can draft legislation that would make the use of digital currencies illegal to be able to stop their operations. This concern among users has now lessened as more and more organizations start to use cryptocurrencies in their operations. One example of this is PayPal, which is a giant online payment processor.

Final thoughts

While there are cases for and against blockchain technology, it appears the pros still outweigh the cons. Perhaps, this is the reason why blockchain continues to exist even to this day. Businesses are starting to see the power of this technology to bring about positive changes in the world. Others say cryptocurrencies may go, but blockchain will stay.